In 2025, global energy, food, and metals markets face mixed outlooks amid geopolitical risks, trade policy shifts, and supply dynamics. Oil prices are expected to remain moderate as supply outpaces demand, though sanctions and OPEC+ cuts could drive volatility. Prices of major crops are set to trend lower, but weather conditions and trade policies remain key factors to watch. Meanwhile, metals markets remain stable but face uncertainty from weaker Chinese demand and changing US trade policy.

Well-supplied oil markets to cap price growth, but trade and policy risks loom

Energy markets entered 2025 with heightened volatility, driven by risks associated with tariffs and sanctions, alongside colder weather conditions driving up demand. Despite the spike in January, however, energy prices are still projected to average lower in 2025, particularly for oil, with supply outpacing demand. Yet, geopolitical risks, escalating trade tensions and policy shifts in key economies remain key upside factors.

Global oil demand is expected to increase modestly this year, accelerating from 2024. China will remain the primary driver of global demand, though its slower economic momentum may temper this growth. Meanwhile, India and other emerging Asian economies will continue to gain prominence in global oil consumption, contributing roughly 45% of the global demand growth in 2025, according to the International Energy Agency. Despite this, underwhelming global growth and broader economic uncertainty is set to keep the global oil market in surplus.

Robust production in non-OPEC+ countries like the US, Canada, and Brazil will help to keep the global oil market well supplied

Source: Euromonitor International

Nonetheless, several factors could provide support for oil prices. OPEC+ continues to enforce a tighter supply policy, with voluntary production cuts in place until at least April 2025. Moreover, potential global oil flow disruptions, particularly from new US sanctions on Russia and Iran, could introduce price volatility and offset downward price pressures.

The outlook for natural gas prices remains tilted to the upside. In Europe, rapid storage depletion has been driven by increased heating demand and reduced pipeline flows following the expiration of the Russia-Ukraine transit agreement, which has impacted roughly 5% of Europe’s gas imports. In mid-February, EU gas storage levels dropped to 45%, significantly below the 5-year average, raising concerns about summer replenishment.

In the US, higher natural gas demand due to cold snaps and increased LNG exports have added upward pressure on prices since early 2025. Moreover, the outlook for electricity consumption has improved, supported by the rapid expansion of data centres and the anticipated manufacturing reshoring.

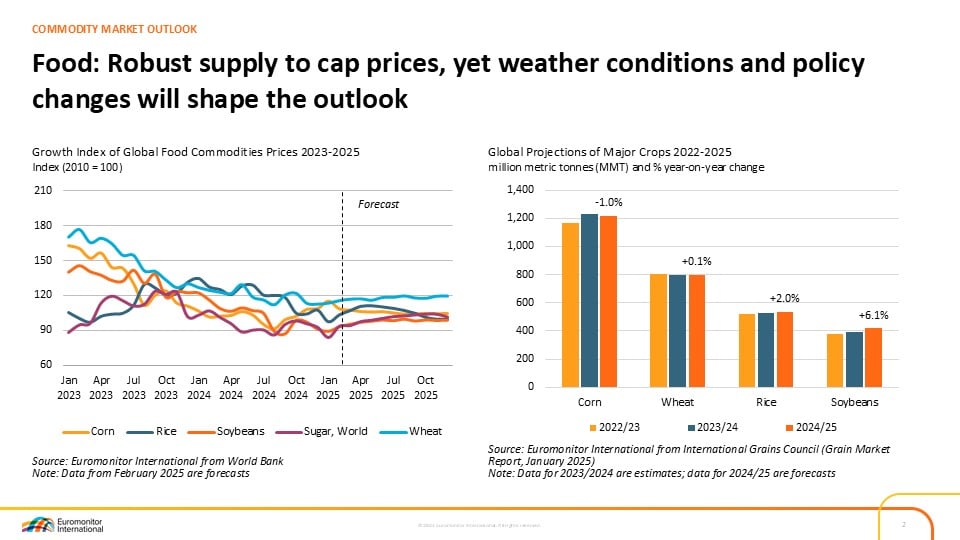

Global food commodity market paints a mixed picture in 2025

In 2025, global agricultural markets will be largely defined by weather conditions, supply dynamics and shifting trade policies, with the outlook diverging across different types of commodities. Corn prices continued to rise in early 2025, fuelled by mounting supply concerns with weaker estimates for US output and global consumption growth. Although corn prices are projected to ease from current levels, limited supply will put upward pressure on them. In contrast, the positive supply outlook has helped to temper wheat and rice prices. India’s rice stocks hit a record high in January, reaching eight times the government’s target, according to the Food Corporation of India, boosting export prospects.

Global sugar prices dropped in January to the lowest level since 2022, thanks to favourable supply in India, which enabled the country to lift export restrictions. However, the risks are tilted upwards, as weak precipitation in Brazil threatens the sugar output and export outlook in 2025. Cocoa prices remain historically high, driven by a global deficit and worsening crop conditions in West Africa, while coffee prices also climbed on supply concerns. Both commodities should ease in 2025 but will remain above historical averages.

Metals market remains stable, yet changes in the US trade policy add more uncertainty

Prices of industrial metals remained generally stable in early 2025, the result of global economic uncertainty, weaker growth in major economies, and improved metal supply. In 2024, global production of aluminium, steel, and copper increased by 2%, while demand stayed moderate, helping to keep the prices in check.

China’s economic performance and export growth will largely determine the trajectory of metal prices in 2025

Source: Euromonitor International

The Lunar New Year and heightened US trade policy uncertainty led to weaker manufacturing sector growth in China, with the official PMI index dropping to 49.1 in January 2025, indicating a contraction. Post-holiday recovery in manufacturing activity and effective stimulus measures could boost China's manufacturing sector and demand for metals. However, harsh US import tariffs on Chinese goods could have lasting negative effects on China’s manufacturing sector, further reducing demand for metals.

Weaker growth of China’s construction sector is also forecast to depress prices of iron ore and steel in 2025. Despite real estate market stabilisation, China’s construction sector is forecast to show slower performance in 2025. For example, floor space of residential construction started in China slumped by 23% in 2024 and reached 2006 levels.

While the overall outlook for metal prices is stable, short-term volatility is likely due to geopolitical tensions and trade uncertainties. The potential EU ban on Russian aluminium imports is already contributing to the higher aluminium prices. Changes in the US trade policy will be another factor to closely monitor in 2025. Overall effects of US tariffs on global metal supply and demand are limited; however, increased price volatility can lead to temporary price spikes, especially in steel, aluminium, nickel and lithium markets.

Read our latest Global Economic Forecasts: Q1 2025 report for more insights on the global outlook and potential implications of Trump’s policy on the global economy.